Riyadh’s airport-linked special zone model is built to make cross-border logistics simpler for international operators. The Saudi Special Integrated Logistics Zone sits next to King Khalid International Airport and is positioned as a platform for regional distribution and trade flows connecting Europe, Asia, and Africa. A key operational feature is immediate airport access through a bonded corridor, intended to remove common transport delays and customs friction. For global 3PLs, that positioning matters because Saudi Arabia’s logistics market is already shifting toward integrated, multi-node networks and long-term outsourcing relationships.

The incentive stack is the headline attraction. Multiple sources describe a 50-year tax exemption structure, including 0% corporate income tax on eligible activities and VAT exemptions. A related framework, the Integrated Logistics Special Bonded Zone (ILBZ), also describes a 50-year tax holiday and states 0% VAT on simple manufacturing, with exemptions maintained when goods are exported outside the Kingdom or moved to another bonded zone. For 3PLs and their clients, these rules can change landed-cost math, especially when the operating model depends on bonded storage, re-export, and postponement-oriented workflows.

What The Bonded-Zone Rulebook Means for Global 3PL Operating Models

The ILBZ rulebook is designed to support cross-border logistics without forcing every activity into mainland structures. It states that non-resident merchants can conduct logistics activities and store goods without the need for a Saudi Commercial Registration (CR) or a permanent establishment on the mainland. The zone is overseen by the General Authority of Civil Aviation (GACA) in coordination with the Zakat, Tax and Customs Authority (ZATCA), and it is described as integrated with airport systems and customs technology. For global 3PLs, that combination supports hub-and-spoke designs that rely on fast air connectivity and bonded handling for onward distribution.

Market signals help explain why bonded and value-added warehousing are getting more attention. Mordor Intelligence values Saudi Arabia’s 3PL warehousing market at USD 3.53 billion in 2025, estimating growth from USD 3.74 billion in 2026 to USD 4.94 billion by 2031 at a 5.71% CAGR (2026–2031). In that same market view, general shared warehousing held 53.09% share in 2025, while bonded warehousing is projected as the fastest-growing warehouse type at a 7.72% CAGR through 2031. Value-added services are also expected to expand quickly, with the highest projected CAGR of 8.55% through 2031.

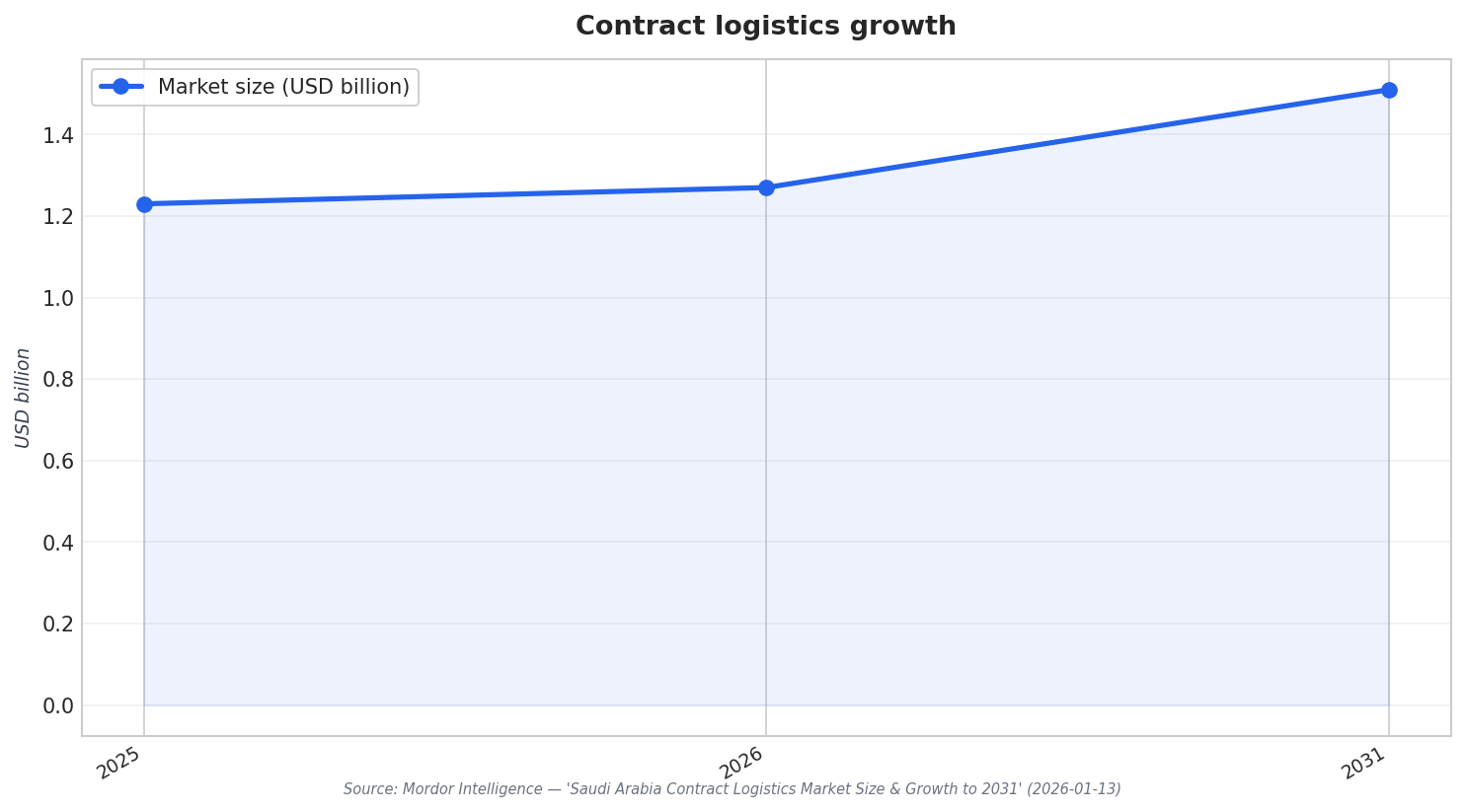

Saudi Arabia’s broader contract logistics trajectory aligns with these zone-driven capabilities. Mordor Intelligence values the Saudi Arabia contract logistics market at USD 1.23 billion in 2025 and estimates growth from USD 1.27 billion in 2026 to USD 1.51 billion by 2031 at a 3.52% CAGR (2026–2031). Transportation remained a large revenue anchor with 64.30% share in 2025, but the same source points to momentum in value-added services such as kitting and postponement. It also notes that special economic zones offer 50-year tax holidays that draw foreign manufacturers and spur demand for bonded warehousing, which is directly relevant to 3PLs designing regional distribution centers around airport-linked bonded corridors.

What tax incentives are offered in Riyadh’s Special Integrated Logistics Zone?

How do bonded-zone rules affect goods moving out of Saudi Arabia?

Can non-resident merchants operate in the Integrated Logistics Special Bonded Zone without a Saudi CR?

What is the growth outlook for bonded warehousing in Saudi Arabia’s 3PL market?