GACA airport privatization Saudi 2026 is landing at a moment of visible strain and opportunity. Saudi Arabia’s civil aviation industry entered 2026 after 2025 recorded passenger traffic of more than 140 million, a 9% increase from the previous year, according to GACA. In the same period, GACA President Abdulaziz Al-Duailej highlighted rising global connectivity, with international destinations now at 176 and three of the world’s busiest air routes continuing to operate through Saudi hubs. Those facts shape the logic of a concession pipeline: capacity is under pressure, connectivity is expanding, and the policy posture is explicitly pro-competition and pro-investment.

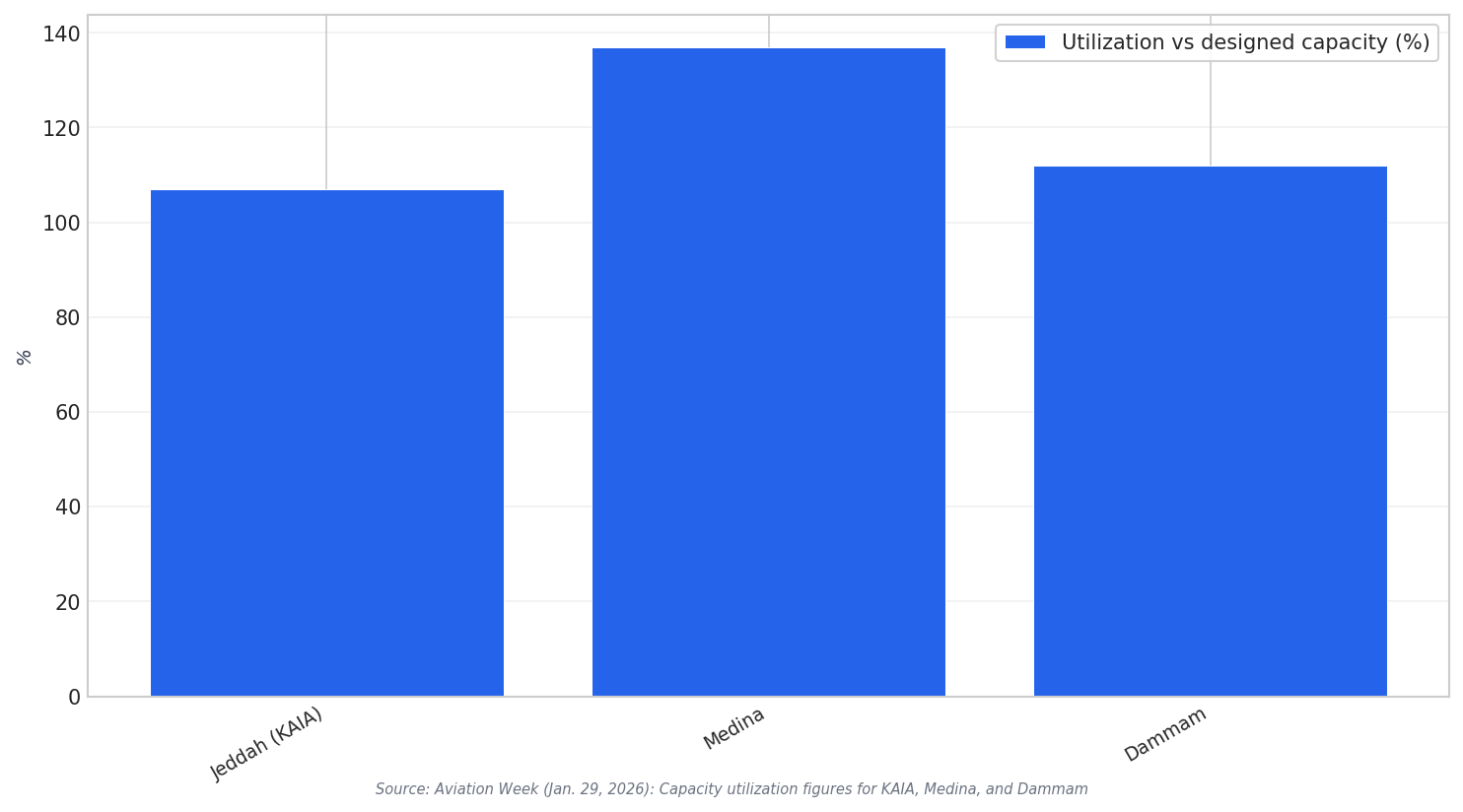

The operational pressure is most visible in utilization and daily throughput at major gateways. King Abdulaziz International Airport in Jeddah remained the nation’s busiest and handled 38% of all passengers, averaging 146,000 travelers per day. It also surpassed its designed capacity by 107%. King Khalid International Airport in Riyadh served 29% of passengers at 112,000 daily. Prince Mohammad bin Abdulaziz International Airport in Medina and King Fahd International Airport in Dammam reported utilization rates of 137% and 112%, respectively. These figures help explain why GACA’s 2026 language centers on capacity and delivery, not just vision statements.

What GACA Says the 2026 Concession Push Must Deliver

In its 2026 outlook, GACA said it intends to empower the private sector in airport development, boost overall capacity, and launch more than 30 new domestic and international routes. It also said special attention will be given to operational readiness and deploying national workforce talent to support pilgrims during Hajj and Umrah. For concessionaires, that reads like a performance agenda: expand capacity, keep service levels stable, and support peak pilgrimage demand. It also aligns with GACA’s broader goal of fostering a competitive aviation environment and attracting international investment, which Al-Duailej emphasized as a core national commitment.

Signals of “market opening” sit alongside the airport story, reinforcing the investment narrative around GACA airport privatization Saudi 2026. In May 2025, GACA abolished cabotage flight restrictions for air charter operators, allowing foreign on-demand providers to apply to fly between Saudi cities as well as in and out of the country. After that shift, GACA approved VistaJet to offer commercial flights within the country, and later granted Malta-based AirX Charter a foreign operator authorization under GACAR Part 129 to begin on-demand flights within the kingdom. GACA leadership framed these approvals as enhancing competition and strengthening service quality, which can matter to bidders assessing demand depth and regulatory direction.

Airport corporatization and project pipelines also provide context for how concessions may be structured and delivered. Aviation Week reports JEDCO was established in 2022 as part of Saudi Arabia’s aviation sector privatization program, with KAIA in Jeddah handling 53.4 million passengers during 2025. Separately, Riyadh’s King Salman International Airport (KSIA) has a mega terminal planned to span several million square feet, with construction scheduled to start in 2026, including new aircraft hangars and airside infrastructure. And on the planning side, Matarat appointed Mott MacDonald to update masterplans for 25 airports over a two-year period, covering future demand, facility capacity, land use, and implementation strategies including infrastructure upgrades. Together, these elements frame a practical runway for concessions: masterplans, construction starts, and privatization vehicles already in motion.

What does “GACA airport privatization Saudi 2026” refer to in official messaging?

Which airports show the strongest capacity pressure in the cited data?

What passenger-traffic figure sets the backdrop for the 2026 concession pipeline?

How has GACA supported competition beyond airports?

What planning and delivery work suggests projects will move in 2026?